Post-Closing Trial Balance

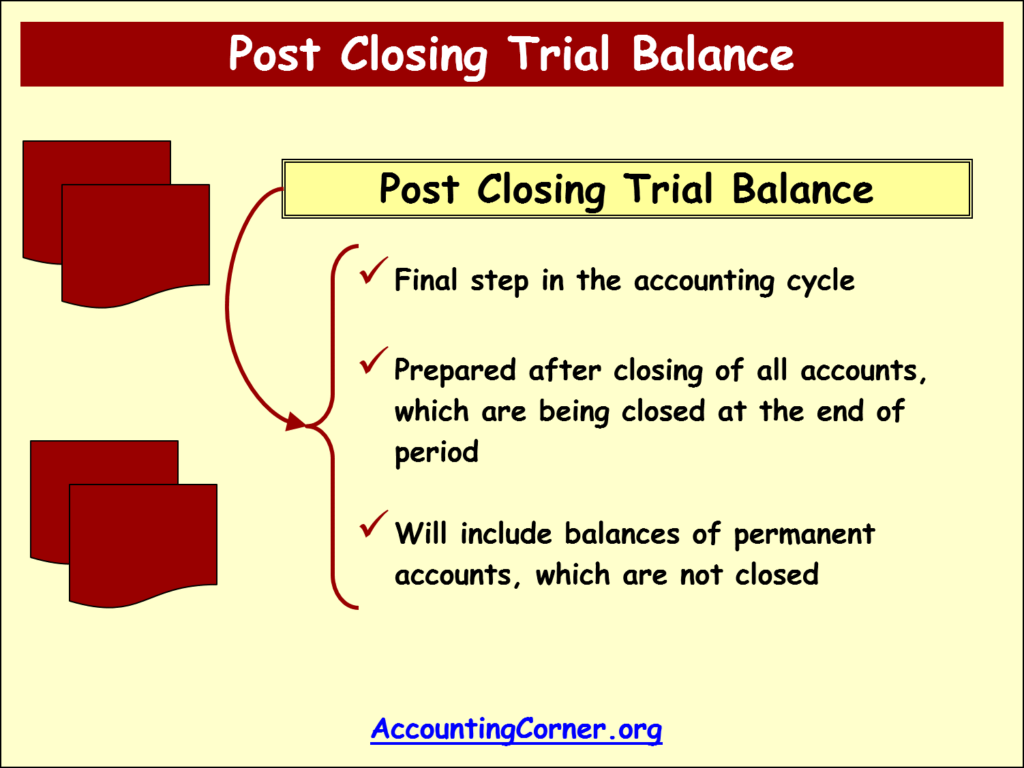

A post-closing trial balance is a financial statement that contains the balances of all accounts in a company's general ledger after the closing entries have been made at the end of an accounting period. It is prepared after the closing entries are made to ensure that the books are balanced and that all temporary accounts have been properly closed.

Here are some key points about the post-closing trial balance:

Timing: The post-closing trial balance is prepared after the closing entries have been made at the end of the accounting period. Closing entries are journal entries made to transfer the balances of temporary accounts (such as revenue, expenses, and dividends) to the permanent accounts (such as retained earnings).

Purpose: The primary purpose of the post-closing trial balance is to verify that the closing entries have been made correctly and that the balances of all accounts are accurate. It helps ensure that the company's books are in balance and that there are no errors in the closing process.

Content: The post-closing trial balance includes the balances of all accounts in the general ledger, both permanent (or real) accounts and temporary (or nominal) accounts. Permanent accounts, such as assets, liabilities, and equity accounts, should have non-zero balances, while temporary accounts should have zero balances after the closing entries are made.

Format: The format of the post-closing trial balance is similar to that of a regular trial balance. It typically consists of three columns: one for the account names, one for the debit balances, and one for the credit balances. The total debits should equal the total credits, indicating that the books are balanced.

Adjustments: If errors are discovered in the post-closing trial balance, adjustments may need to be made to correct them. This may involve making correcting journal entries to rectify any mistakes or discrepancies in the account balances.

In summary, the post-closing trial balance is a financial statement prepared after the closing entries have been made to verify that the company's books are in balance and that all temporary accounts have been properly closed for the accounting period. It plays a crucial role in ensuring the accuracy and integrity of the company's financial records.

Thank you,